Understanding the fundamental accounting concepts of increasing and decreasing asset values. A crucial distinction impacting financial records and decisions.

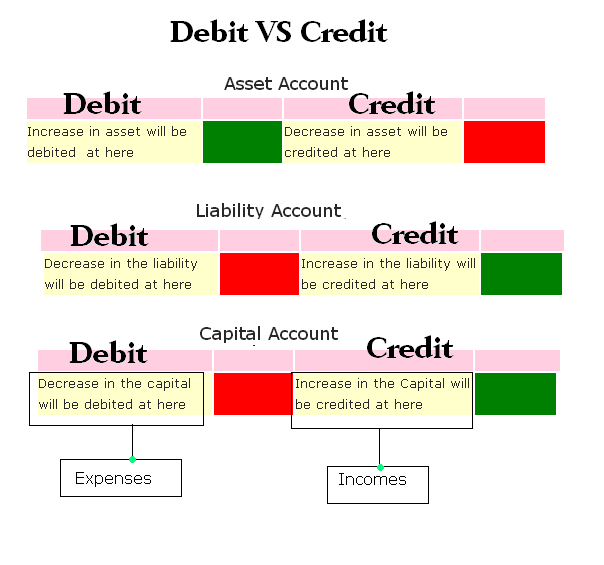

Accounting employs two fundamental concepts: increasing and decreasing asset values. A credit signifies an increase in liabilities or owner's equity, or a decrease in assets. Conversely, a debit signifies a decrease in liabilities or owner's equity, or an increase in assets. For instance, receiving cash from a customer increases cash (an asset) and decreases the account receivable. This would be recorded as a debit to cash and a credit to accounts receivable. Conversely, if paying an expense, the cash balance would decrease, which is a debit, and the expense account would increase, which is a credit. These seemingly simple entries form the bedrock of all financial reporting.

The distinction between credit and debit is fundamental to accurate financial record-keeping. Proper application ensures that the accounting equation (Assets = Liabilities + Equity) consistently balances. This balancing act is crucial for informed decision-making. Understanding credits and debits enables businesses to track income, expenses, assets, and liabilities, facilitating financial planning, analysis, and reporting. Effective use of this system is crucial for regulatory compliance, shareholder reporting, and overall business health.

Moving forward, we will delve into specific application examples in accounting to demonstrate the practical implementation of these concepts. We will illustrate their impact on profitability, liquidity, and solvency within a dynamic business context. A clear understanding of this framework is essential for anyone interested in grasping the principles of financial accounting.

Credit vs Debit

Understanding the distinction between credit and debit is fundamental to accurate financial record-keeping and informed decision-making. These concepts are crucial for maintaining the integrity of financial statements.

- Asset increase

- Liability decrease

- Equity increase

- Expense decrease

- Revenue increase

- Account balance

- Accounting equation

- Financial reporting

Credits and debits are essential components of the accounting equation, reflecting increases and decreases in various account types. For example, a credit to a revenue account signifies an increase in revenue. Conversely, a debit to an expense account signifies an increase in expenses. Understanding these affects the balance sheet, income statement, and cash flow statement. The accounting equation (Assets = Liabilities + Equity) must always balance. This system ensures accurate financial reporting, crucial for businesses to assess performance, make informed decisions, and meet regulatory requirements. Imbalances in debits and credits can lead to inaccurate financial statements, hindering a company's ability to make sound business decisions.

1. Asset Increase

An increase in assets is a fundamental aspect of accounting. Its relationship with credits and debits is crucial for maintaining accurate financial records. A debit entry typically signifies an increase in an asset account. For example, if a company receives cash from a customer, the cash account (an asset) increases. This increase is reflected by a debit entry to the cash account. Similarly, if a company purchases equipment, the equipment account (an asset) increases, and this increase is recorded with a debit entry.

Conversely, while a credit entry does not directly result in an increase in assets, it often accompanies transactions that indirectly impact asset values. For example, if a company takes out a loan, the loan is recorded as a liability, and this would be a credit entry to the liability account. However, cash (an asset) also increases as a result of the loan. In this instance, the credit entry reflects the increase in the loan account and, simultaneously, the debit entry reflects the increase in cash. The core of the accounting equation (Assets = Liabilities + Equity) mandates a balancing act. This balancing act ensures that for every transaction, assets, liabilities, and equity have to be in balance. Maintaining this balance is vital for ensuring accurate financial statements and for informed decision-making.

Understanding the connection between asset increases and debits is vital for creating reliable financial records. It enables a comprehensive view of the financial health of a business, revealing where resources are coming from (cash inflows), and how those resources are being used (asset acquisitions). Precise tracking of these increases and decreases in asset values is fundamental to evaluating the financial performance and position of a business, providing insights crucial for financial planning, investment decisions, and regulatory compliance.

2. Liability Decrease

Liability decrease is a critical accounting concept directly related to the principles of credit and debit. Understanding how decreases in liabilities are recorded and reflected in financial statements is essential for accurate financial reporting and informed decision-making. This process ensures the accounting equation (Assets = Liabilities + Equity) remains balanced. The precise application of credit and debit entries during liability decreases ensures a consistent and reliable representation of a company's financial position.

- Impact on the Accounting Equation

A decrease in liabilities results in a corresponding decrease in the total of the right-hand side of the accounting equation. This decrease, in turn, maintains the balance between the assets and the combined total of liabilities and equity. For example, if a company repays a loan, the liability decreases, and a credit entry reduces the loan balance. Simultaneously, a corresponding debit entry is made to the cash account. This maintains the balance, showcasing the financial effect of the repayment.

- Specific Examples of Liability Decreases

Various transactions can lead to liability decreases. Payment of accounts payable (amounts owed to suppliers) decreases liabilities. Repaying a short-term loan also reduces liabilities. The crucial aspect is that every reduction in liabilities is reflected by an appropriate credit entry in the relevant liability account and a corresponding debit entry elsewhere in the accounting equation.

- Significance in Financial Reporting

Accurate representation of liability decreases is paramount for transparent financial reporting. Investors, creditors, and other stakeholders rely on these figures to assess the financial health and stability of a company. A precise understanding of liabilities and their decrease, reflected through debits and credits, empowers stakeholders to make informed judgments.

- Relationship with other Accounts

Liability decreases frequently correlate with changes in other accounts. For instance, repaying a loan reduces the loan liability and simultaneously increases the cash account (an asset). Understanding this interconnectedness within the accounting system is crucial for maintaining accurate records.

In conclusion, liability decreases, like all accounting transactions, are meticulously tracked using credits and debits. This method ensures the integrity and accuracy of financial reporting. This allows for insightful analysis of a company's financial health and performance by stakeholders. The precise handling of liability decreases strengthens the validity and reliability of the entire financial picture.

3. Equity Increase

Equity increase represents an augmentation of a company's net worth. This increase is a critical accounting concept directly linked to credit and debit entries. Understanding this connection is essential for accurate financial reporting and informed decision-making.

- Impact on the Accounting Equation

An increase in equity directly impacts the accounting equation (Assets = Liabilities + Equity). A credit to equity accounts, such as retained earnings, reflects this increase. Conversely, a debit to these accounts would signify a decrease in equity, maintaining the equation's balance.

- Sources of Equity Increase

Several transactions can contribute to equity augmentation. Profit from operations, investment gains, and owner contributions all increase equity. In each instance, the corresponding credit entries to equity accounts accurately reflect these positive developments, highlighting their influence on the overall financial well-being of the company.

- Relationship with Debits and Credits

The relationship between equity increases and credit entries is integral. The credit entries represent the inflow of resources that enhance the company's net worth. Debits, on the other hand, play a role in reducing equity through expenses and dividends, although not directly causing an increase. These debit entries, when analyzed in conjunction with the accompanying credit entries, present a comprehensive picture of equity fluctuations. This meticulous record-keeping enables a clear understanding of how various transactions impact the financial health of the business.

- Examples of Transactions Affecting Equity

Consider the case of a company earning profits. The revenue generated from business operations leads to an increase in equity. This increase is reflected by a credit to retained earnings. Similarly, contributions from shareholders directly increase equity. These transactions accurately reflect the growing value of the company, showcasing the impact on the accounting equation and providing insights into the company's financial performance.

In summary, increases in equity are crucial components of financial statements. The use of credits to reflect these increases, paired with a comprehensive understanding of corresponding debit entries, provides a clear, balanced view of the company's financial position. This, in turn, allows for informed decision-making related to future investments, operations, and overall strategic planning.

4. Expense Decrease

Expense decrease, a significant element in financial accounting, is intrinsically linked to the concepts of credit and debit. Accurate recording of expense decreases through proper application of debits and credits ensures the integrity of financial statements, facilitating informed decision-making and strategic planning.

- Impact on the Accounting Equation

A decrease in expenses, like any financial transaction, affects the accounting equation (Assets = Liabilities + Equity). Decreasing expenses results in an increase in net income, thus increasing equity. This is reflected by a corresponding credit entry to the expense account and a debit entry to a related account, such as retained earnings or a revenue account, to maintain the equation's balance. For example, if a company negotiates a reduction in supplier costs, the corresponding expense account decreases. This decrease is recorded as a credit, and the corresponding increase in available cash (or equivalent) is recorded as a debit to the appropriate asset account.

- Specific Examples of Expense Decreases

Numerous situations can lead to expense reductions. Negotiating lower rent payments, streamlining operations to reduce labor costs, or implementing energy-saving measures all result in expense decreases. Each scenario necessitates adjusting the relevant expense accounts on the income statement. This adjustment, using credit and debit entries, preserves the accuracy of the financial records. For instance, if utility costs decrease, the utility expense account would be credited, reflecting the decrease.

- Relationship with Revenue and Profitability

Expense decreases directly correlate with increased profitability. By lowering expenses without significantly impacting revenue, companies enhance their net income. This improved profitability is reflected in the financial statements and can be a crucial indicator of a company's financial health. The proper recording of these decreases, using credit entries to the expense accounts and corresponding debit entries to other accounts, ensures an accurate reflection of this positive impact on the bottom line.

- Application in Financial Reporting

Accurate representation of expense decreases in financial statements is vital for transparency. Investors, creditors, and other stakeholders rely on these reports to evaluate a company's financial performance. Precise application of credit and debit entries ensures that the financial impact of these reductions is correctly reflected, enabling informed assessments and strategic decision-making by stakeholders, as well as regulatory compliance.

In conclusion, expense decreases, through the application of credit and debit entries, directly impact financial statements, reflecting on a company's profitability and financial health. A clear understanding of these principles ensures accurate representation and facilitates informed decisions by various stakeholders. This precise record-keeping underscores the importance of maintaining the integrity of financial information.

5. Revenue Increase

Revenue increase is a pivotal aspect of financial performance, intrinsically linked to the accounting principles of credit and debit. Accurate recording of revenue increases, utilizing the correct application of credit and debit entries, ensures the integrity of financial statements and facilitates informed decision-making. This process directly impacts a company's profitability and overall financial health.

- Impact on the Accounting Equation

An increase in revenue directly influences the accounting equation (Assets = Liabilities + Equity). A credit to revenue accounts reflects this increase. This credit, in turn, elevates the equity portion of the equation, thereby increasing the overall net worth of the entity. Simultaneously, a debit entry is recorded to a corresponding account (often cash or accounts receivable), reflecting the increase in assets resulting from the revenue generation. This debit entry maintains the balance within the accounting equation.

- Types of Revenue Increases

Revenue increases manifest in diverse forms. Sales of goods or services, interest earned, and gains from investments are all examples. Each type of revenue increase necessitates a specific accounting treatment, meticulously documented via credit and debit entries. The precise method of accounting distinguishes between different revenue streams, highlighting variations in financial impact.

- Relationship with Credits and Debits

The application of credits and debits is crucial to accurately representing revenue increases. A credit to a revenue account reflects an increase in that revenue. This credit entry mirrors an increase in equity (because revenue increases net worth). The corresponding debit entry acknowledges the associated increase in assets or reduction in liabilities. This methodical recording ensures a balanced accounting equation and a consistent reflection of financial reality.

- Examples and Implications

Consider a retail store selling merchandise. Sales generate revenue, and this increase in revenue necessitates a credit to the sales revenue account. Concurrently, the cash account (an asset) increases, requiring a corresponding debit entry to that account. This intricate link between revenue increases, credits, and debits allows for accurate tracking of financial performance, underpinning critical business decisions, such as pricing strategies and inventory management.

In summary, revenue increases, when correctly documented via credit and debit entries, provide a clear picture of a company's financial position and performance. The accurate application of these accounting principles ensures the integrity of financial statements, facilitating informed decision-making and strategic planning, and ultimately, maintaining a comprehensive overview of the organization's financial health.

6. Account Balance

Account balance, a fundamental concept in accounting, directly reflects the impact of credit and debit entries. Understanding this relationship is essential for accurate financial record-keeping and informed decision-making. A clear account balance reveals the net effect of all transactions, highlighting the current state of an account, and is crucial for maintaining the integrity of financial statements. The balance acts as a critical check against inaccuracies and errors, ensuring the reliability of financial information.

- Impact of Credits and Debits

Credits and debits are the fundamental building blocks of account balances. A credit increases a liability, owner's equity, or revenue account, whereas a debit increases an asset or expense account. These increases or decreases, meticulously documented through entries, directly influence the balance. For example, a credit to a customer's account increases the balance, reflecting the growing receivable amount. Conversely, a debit to a company's cash account signifies the decrease in that asset.

- Maintaining the Accounting Equation

The relationship between credits and debits is vital for maintaining the fundamental accounting equation (Assets = Liabilities + Equity). Each transaction, whether a credit or a debit, must affect the equation. Account balances, derived from the accumulation of these entries, directly contribute to the accuracy of this equation. An unbalanced equation often indicates an error in record-keeping, highlighting the critical role of accurate credits and debits in achieving a correct account balance.

- Error Detection and Prevention

An accurate account balance acts as a crucial internal control mechanism. Regularly reconciled balances help detect errors or inconsistencies in transactions. Significant discrepancies between expected and actual balances necessitate investigation, allowing for the identification and correction of potential errors before they escalate. This proactive approach safeguards the integrity of financial information and prevents inaccuracies that could negatively impact decision-making.

- Decision Support and Analysis

Account balances offer critical insights for decision-making. The balance in an account for sales, for example, indicates the volume of business conducted. The balance in an expense account reveals the incurred costs. Analyzing account balances across different periods enables trend identification, allowing businesses to assess growth patterns, predict future trends, and identify areas for improvement. This analysis strengthens the basis for strategic planning and resource allocation.

In conclusion, account balances are not merely numerical figures but essential indicators of financial health. The underlying connection between account balances and credit/debit entries is paramount. Precise and timely recording of transactions, accurate calculation of balances, and thorough reconciliation processes are vital for ensuring the reliability and accuracy of financial information. This, in turn, underpins critical decision-making processes for businesses and organizations.

7. Accounting Equation

The accounting equation, a fundamental principle in accounting, forms the bedrock of financial reporting. It establishes a crucial relationship between assets, liabilities, and equity. This equation, Assets = Liabilities + Equity, underscores the balance inherent in financial records. The concepts of credit and debit are integral components in maintaining this equation's integrity and accurately reflecting the financial state of an organization.

- Assets, Liabilities, and Equity: Fundamental Components

Assets represent the resources owned by an entity, encompassing items like cash, accounts receivable, and property. Liabilities denote the company's obligations to external parties, including accounts payable, loans, and deferred revenue. Equity reflects the residual interest in the assets after deducting liabilities. The accounting equation ensures that the sum of all liabilities and equity always equals the value of assets. This balance is crucial for financial analysis and decision-making. The application of debits and credits is essential for tracking the changes in these components, ensuring accuracy and consistency.

- Debits and Credits: Maintaining Balance

Every financial transaction impacts assets, liabilities, or equity. Debits and credits are used to record these transactions. A debit increases asset and expense accounts, while decreasing liability and equity accounts. A credit increases liability, equity, and revenue accounts, and decreases asset accounts. For instance, a cash inflow increases an asset (cash), and this is reflected with a debit to the cash account. Conversely, an outflow decreases cash, demanding a credit to the cash account. Maintaining this system of credits and debits ensures that the accounting equationAssets = Liabilities + Equityremains balanced after each transaction.

- Example of Transaction Impact

Consider a company purchasing equipment for $10,000 using cash. This transaction affects both the asset (cash) and the asset (equipment) accounts. The equipment account increases by $10,000 (debit), reflecting the acquisition of the asset. Simultaneously, the cash account decreases by $10,000 (credit), reflecting the outflow of cash. Through these debit and credit entries, the accounting equation remains balanced, accurately reflecting the shift in the company's assets. This exemplifies how debits and credits are used to adjust the equation and maintain financial record accuracy.

- Significance in Financial Reporting

The accounting equation and the related principles of credit and debit are foundational to financial reporting. The balance they represent provides a snapshot of an entity's financial health and position. Investors, creditors, and regulatory bodies rely on this accurate and consistent reporting to assess financial performance, make informed decisions, and maintain the integrity of the financial system. Any violation of these principles could lead to inaccurate financial statements and hinder informed judgments.

In conclusion, the accounting equation acts as a crucial framework for recording financial transactions. The principles of credit and debit are vital for maintaining the accuracy and integrity of this equation. The interconnectedness of these concepts ensures the reliability of financial reporting, facilitating informed decision-making and promoting trust in financial markets.

8. Financial Reporting

Financial reporting relies fundamentally on the accurate application of credit and debit entries. These entries form the basis for recording all financial transactions, whether reflecting revenue generation, expense incurrence, or changes in assets, liabilities, and equity. The meticulous use of debits and credits ensures that the accounting equation (Assets = Liabilities + Equity) remains balanced. Maintaining this balance is crucial for producing reliable financial statements. Inaccurate recording of transactions, through flawed application of credits and debits, leads to distorted financial reports. This distortion, in turn, hinders informed decision-making, potentially misrepresenting the true financial health of an organization.

Consider a company's sales transaction. When goods are sold, revenue increases. This increase in revenue is recorded as a credit. Simultaneously, the cash account or accounts receivable (both assets) increases, recorded as a debit. Accurate recording of both sides of this transaction, using credits and debits, ensures an accurate depiction of the company's revenue and its effect on assets. Similarly, when a company pays for expenses, the cash account decreases, requiring a debit entry to the cash account. The expense account increases, requiring a credit entry. This system meticulously tracks the inflow and outflow of funds, providing a clear picture of the company's financial activities. External stakeholders, such as investors and creditors, utilize these financial reports to assess a company's performance and financial soundness. Distortions in these reports due to errors in credit and debit application can lead to misleading assessments, jeopardizing investment decisions and creditworthiness.

Precise application of credits and debits is essential for accurate financial reporting. This accuracy is crucial for effective decision-making by internal management and external stakeholders. The reliability of financial statements hinges on the meticulous recording of every transaction using debits and credits. Errors in this fundamental recording process undermine the trustworthiness of financial reports and potentially hinder prudent financial planning and investment decisions. Organizations committed to transparency and accountability must maintain strict adherence to proper credit and debit application to ensure accurate financial reporting. This accurate reporting fosters trust amongst stakeholders and facilitates informed decisions that drive sustainable business growth and overall financial success.

Frequently Asked Questions

This section addresses common questions regarding the fundamental accounting concepts of credit and debit. Clear understanding of these concepts is crucial for accurate financial record-keeping and informed decision-making.

Question 1: What is the difference between a credit and a debit?

A credit increases liability, owner's equity, or revenue accounts, and decreases asset accounts. A debit increases asset and expense accounts, and decreases liability and equity accounts. These opposing effects are essential for maintaining the fundamental accounting equation (Assets = Liabilities + Equity).

Question 2: How do credits and debits affect the balance sheet and income statement?

Credits and debits impact both statements. On the balance sheet, credits increase liabilities and owner's equity, while debits increase assets. On the income statement, credits increase revenues and decrease expenses, impacting net income, which in turn affects equity on the balance sheet.

Question 3: Why is it important to record transactions using credits and debits accurately?

Accurate recording is essential for maintaining the integrity of financial statements. Inaccurate use of credits and debits can lead to an unbalanced accounting equation, misrepresenting an organization's financial position. This misrepresentation hinders informed decision-making by stakeholders.

Question 4: What are some common errors related to credits and debits?

Common errors include incorrect account identification, incorrect debit/credit application, and overlooking the impact of transactions on multiple accounts. Careless application can lead to discrepancies and inaccuracies in financial reports. Thorough review and double-checking procedures are critical to avoid these errors.

Question 5: How can I ensure proper application of credits and debits in my financial records?

Adherence to established accounting principles and procedures is vital. Comprehensive training, using resources like accounting manuals and software, facilitates proper application. Consistent double-checking and review procedures are necessary to identify and correct potential errors. Maintaining a system of internal controls to monitor transactions is also crucial.

A clear understanding of the principles of credit and debit is essential to financial success. These seemingly simple concepts underpin accurate financial record-keeping and informed decision-making within any organization.

Next, we will delve into specific examples illustrating the practical application of these concepts.

Conclusion

The concepts of credit and debit are fundamental to accurate financial record-keeping. This exploration has highlighted the critical role these entries play in maintaining the integrity of the accounting equation (Assets = Liabilities + Equity). The meticulous application of credits and debits ensures an accurate reflection of financial transactions, impacting various aspects of a company's operations, from revenue generation to expense management. The principles outlined demonstrate how every transaction, whether a sale, payment, or investment, necessitates corresponding debit and credit entries to maintain the equation's balance. Proper application prevents inconsistencies that could distort financial reports and undermine informed decision-making.

Accurate financial reporting, facilitated by a thorough understanding of credit and debit entries, is paramount for effective business operations. This accuracy enables informed decisions concerning resource allocation, investment strategies, and overall financial planning. The reliability of financial statements, built on the bedrock of precise credit and debit application, underpins trust among stakeholders and contributes to a sound financial system. Maintaining this accuracy is crucial not only for internal management but also for external stakeholders relying on these reports to assess financial health and performance.

Article Recommendations

- Does Adele Have Any Little Monsters Uncovering The Truth Behind Her Kids

- The Truth About Lance Barbers Shocking Weight Loss

- Discover More Katie Findlays Precious Little Ones

:max_bytes(150000):strip_icc()/dotdash-050214-credit-vs-debit-cards-which-better-v2-02f37e6f74944e5689f9aa7c1468b62b.jpg)