Understanding the fundamental accounting concept of debits and credits is crucial for accurate financial reporting and record-keeping. Mastering their distinctions is essential for any individual involved in the accounting process.

In accounting, debits and credits are used to record transactions. They represent increases and decreases in different account types. A debit increases asset, expense, and dividend accounts, while it decreases liability, owner's equity, and revenue accounts. Conversely, a credit increases liability, owner's equity, and revenue accounts, and decreases asset, expense, and dividend accounts. Consider a transaction where a business purchases supplies for $100 in cash. The cash account, an asset, is decreased, thus requiring a debit. The supplies account, also an asset, is increased, requiring a credit. This duality is essential for maintaining the fundamental accounting equation: Assets = Liabilities + Equity.

The importance of understanding this fundamental concept extends beyond basic bookkeeping. Accurate recording of debits and credits forms the bedrock of financial statements like the balance sheet and income statement. These statements provide a snapshot of a company's financial health, allowing stakeholders like investors, creditors, and management to make informed decisions. Moreover, proper application of debits and credits ensures that transactions are recorded accurately, preventing errors and inconsistencies in financial reports. Historical accounting practices have consistently relied on this duality to maintain the integrity and reliability of financial data.

Moving forward, let's explore specific examples of how debits and credits are used in various accounting scenarios. Further, we will examine practical applications and common pitfalls in debit and credit usage.

Difference Between Debit and Credit in Accounting

Understanding the distinction between debits and credits is fundamental to accurate accounting. This knowledge ensures reliable financial reporting and informed decision-making.

- Account Types (e.g., assets, liabilities)

- Increase/Decrease (e.g., asset increase, liability decrease)

- Balance Sheet (e.g., asset side, liability side)

- Transaction Impact (e.g., purchase, sale)

- Equation Balance (e.g., assets=liabilities+equity)

- Financial Statements (e.g., balance sheet, income statement)

- Journal Entries (e.g., debit, credit)

- Accounting Principles (e.g., GAAP, IFRS)

These aspects are interconnected. For example, a sale increases revenue (credit) and decreases cash (debit). The debit and credit balancing in journal entries maintains the fundamental accounting equation. The correct application of debits and credits ensures accurate financial statements, which, in turn, provide a clear picture of a company's financial health. Understanding how debits and credits impact various account types across financial statements is vital for any accounting professional.

1. Account Types (e.g., assets, liabilities)

Account types are fundamental to understanding the difference between debits and credits. The nature of an account dictates how a transaction affects it, influencing the use of debit and credit entries. Different account types, such as assets, liabilities, and equity, have distinct characteristics that determine their treatment in recording financial events.

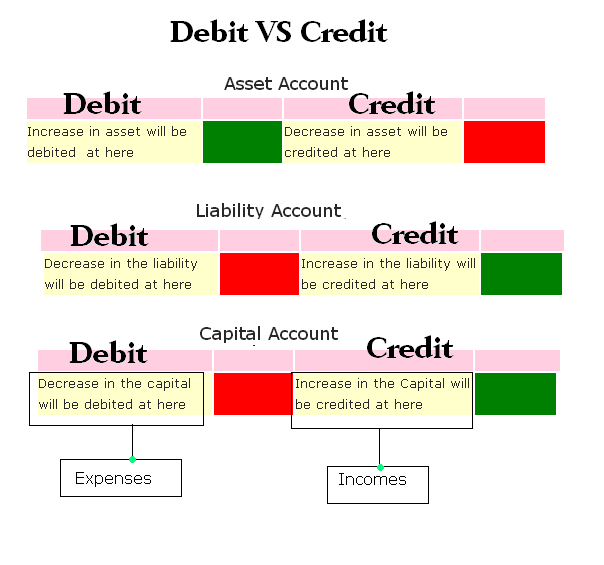

- Assets

Assets represent a company's resources. Examples include cash, accounts receivable, inventory, and equipment. An increase in an asset account is recorded with a debit. Conversely, a decrease in an asset account is recorded with a credit. For example, if a company purchases equipment, the equipment account (an asset) increases, necessitating a debit. Conversely, if the company sells equipment, the equipment account decreases, requiring a credit. This consistent application is crucial for maintaining an accurate record of assets.

- Liabilities

Liabilities represent a company's obligations to others. Examples include accounts payable, salaries payable, and loans payable. An increase in a liability account is recorded with a credit. A decrease in a liability account is recorded with a debit. For instance, if a company incurs a debt by taking out a loan, the loan payable account (a liability) increases, necessitating a credit. If the company repays a portion of the loan, the loan payable account decreases, requiring a debit. These entries ensure liabilities are accurately reflected in financial records.

- Equity

Equity represents the residual interest in the assets of the entity after deducting its liabilities. Common equity accounts include contributed capital and retained earnings. Increases in equity are recorded with credits, while decreases are recorded with debits. For example, if a company issues new shares of stock, contributed capital increases, resulting in a credit. If the company incurs a net loss, retained earnings decrease, requiring a debit. These transactions maintain the balance of the accounting equation.

Understanding the characteristics of these account types is integral to applying the correct debit or credit entry. The relationship between account type and debit/credit application forms the cornerstone of the accounting process. Accurate categorization ensures that financial statements reflect the true financial position and performance of a company.

2. Increase/Decrease (e.g., asset increase, liability decrease)

The relationship between increases and decreases in accounts and the application of debits and credits is fundamental to accounting. Understanding how these factors interact is vital for accurate financial record-keeping and reporting. An increase in an asset account is always paired with a decrease in another account, maintaining the balance of the accounting equation. Similarly, an increase in a liability or equity account is always accompanied by a decrease in another, preserving the equation's balance. This cause-and-effect relationship is intrinsically linked to the distinction between debits and credits.

Consider an example: A company purchases supplies for cash. The supplies account (an asset) increases, requiring a debit. Simultaneously, the cash account (also an asset) decreases, necessitating a credit. These mirrored actions ensure that the accounting equation (Assets = Liabilities + Equity) remains balanced. If the purchase were recorded incorrectly, the equation would be unbalanced, leading to inaccurate financial statements. This showcases the critical importance of recognizing the increase/decrease relationship for proper application of debit and credit. In another instance, if a company pays off a loan, the cash account (an asset) decreases (debit), and the loan payable account (a liability) decreases (credit). This demonstrates the consistent interplay of increases and decreases in various account types and their corresponding debit/credit entries.

The practical significance of this understanding cannot be overstated. Accurate recording of increases and decreases, facilitated by correct debit and credit application, is critical for producing reliable financial statements. These statements are used by investors, creditors, and management to assess financial health, make strategic decisions, and evaluate performance. A failure to grasp the interplay between increases/decreases and debits/credits can lead to inaccuracies in these statements, potentially misrepresenting the financial position and performance of an entity, ultimately impacting decision-making. Thus, understanding the principle of increases and decreases paired with debits and credits is essential for sound financial management.

3. Balance Sheet (e.g., asset side, liability side)

The balance sheet is a fundamental financial statement, presenting a snapshot of a company's financial position at a specific point in time. Its structure, particularly the asset and liability sides, is directly linked to the principles of debits and credits. Understanding this connection is crucial for interpreting financial statements and ensuring accurate reflection of a company's financial health.

- Asset Side:

The asset side of the balance sheet lists a company's resources, including cash, accounts receivable, inventory, property, plant, and equipment. Debits increase asset accounts. Each transaction affecting an asset is recorded with a corresponding debit or credit, ensuring the balance sheet accurately reflects the value of assets. For instance, a purchase of equipment with cash results in a debit to the equipment account (increasing the asset) and a credit to the cash account (decreasing the asset). This maintains the fundamental accounting equation (Assets = Liabilities + Equity).

- Liability Side:

The liability side of the balance sheet lists a company's obligations to external parties. This includes accounts payable, salaries payable, loans, and deferred revenue. Credits increase liability accounts. A transaction like receiving a loan increases the loan payable account (a liability), requiring a credit. Matching debits and credits to transactions affecting liabilities ensures the equation remains balanced. For example, if a company receives a prepayment from a customer, a liability account (deferred revenue) increases, which is recorded with a credit.

- The Importance of Balancing Debits and Credits:

A crucial aspect of the balance sheet's relationship with debits and credits is maintaining the balance between the asset and liability sides. The sum of all debits on the balance sheet must equal the sum of all credits. This balance confirms the accuracy of the accounting records and ensures the fundamental accounting equation is met. Inaccuracies in debit or credit applications would disrupt this balance and lead to a misrepresentation of the company's financial status.

- Relationship to the Accounting Equation:

The balance sheet directly reflects the accounting equation (Assets = Liabilities + Equity). The asset side represents the total assets, and the sum of liabilities and equity on the liability side must equal the total assets. If a companys accounting records correctly apply debits and credits, the equation holds true, signifying the accurate representation of the company's financial position.

In summary, the balance sheet's structure, from its asset and liability sides, is deeply intertwined with the principles of debits and credits. Proper application of these principles ensures the accuracy and reliability of the balance sheet, providing a crucial picture of a company's financial health, directly impacting decision-making and the overall evaluation of its performance. Correctly recording debits and credits is essential to maintain the balance of the balance sheet, which in turn maintains the integrity of the accounting equation.

4. Transaction Impact (e.g., purchase, sale)

Transaction types, such as purchases and sales, directly influence the application of debits and credits in accounting. Understanding these impacts is fundamental for accurate financial record-keeping. A purchase, for example, typically involves an increase in an asset (inventory) and a decrease in another asset (cash). A sale conversely results in an increase in assets (cash) and a decrease in assets (inventory). These changes are meticulously recorded using debits and credits, ensuring the fundamental accounting equation (Assets = Liabilities + Equity) remains balanced. The accurate recording of these transactions is paramount, as errors in applying debits and credits can lead to inaccurate financial statements and subsequently flawed decision-making.

Consider a purchase of raw materials for $1,000 in cash. This transaction impacts two asset accounts: raw materials (increased) and cash (decreased). Recording this purchase correctly requires a debit to the raw materials account (increasing its balance) and a credit to the cash account (decreasing its balance). This ensures the accounting equation remains balanced. Similarly, a sale of finished goods for $1,500 in cash increases the cash account and decreases the inventory account. Recording the sale correctly involves debiting the cash account and crediting the inventory account. Detailed record-keeping of such transactions, utilizing the principles of debits and credits, is crucial for preparing financial statements. Accurate financial statements are vital for stakeholders' assessments of a company's financial health and operational efficiency, ultimately driving informed decision-making.

The practical significance of understanding the impact of transactions on debits and credits cannot be overstated. Accurate recording of purchases and sales, and other transactions, allows for the preparation of reliable financial statements. These statements, including the balance sheet and income statement, are essential tools for investors, creditors, and management. They provide a clear picture of a company's financial position and performance, allowing for informed decisions regarding investments, loans, and operational strategies. Failure to accurately reflect the impact of transactions through debits and credits can result in misleading financial reports, potentially jeopardizing sound business practices and decisions based on flawed information. This underscores the importance of meticulous attention to detail in recording transactions and understanding the corresponding debit and credit entries.

5. Equation Balance (e.g., assets=liabilities+equity)

The fundamental accounting equation, Assets = Liabilities + Equity, forms the bedrock of accounting. Maintaining the balance of this equation is integral to accurate financial reporting. The difference between debits and credits plays a crucial role in upholding this balance, ensuring a faithful representation of a company's financial position.

- Debits and Credits as Balancing Tools:

Debits and credits are not simply bookkeeping entries; they are the mechanisms that ensure the accounting equation remains in balance. Each transaction affects at least two accounts. A debit in one account is always accompanied by a corresponding credit in another account. This duality is critical; it prevents imbalances and maintains the accuracy of financial records. For example, purchasing equipment for cash requires a debit to the equipment account (increasing an asset) and a credit to the cash account (decreasing an asset). The equation's balance is preserved. Similarly, recognizing revenue involves crediting the revenue account (increasing equity) and debiting a corresponding account (such as accounts receivable).

- Maintaining the Equation's Integrity:

The accounting equation's balance is a direct reflection of the fundamental principle of double-entry bookkeeping. By meticulously applying debits and credits to transactions, accountants maintain the integrity of financial records, ensuring assets, liabilities, and equity are accurately and comprehensively represented. If one side of the equation is improperly adjusted, the balance is disrupted, leading to inaccurate financial statements. The correct application of debits and credits thus safeguards the equation's integrity, supporting reliable financial reporting.

- Impact on Financial Statements:

The equation's balance directly influences financial statements. A properly balanced equation ensures the balance sheet's accuracy. The balance sheet, an essential financial statement, presents a snapshot of a company's financial position. If debits and credits are not applied correctly, the balance sheet will not accurately reflect assets, liabilities, and equity. Consequently, the income statement and cash flow statement, derived from the balance sheet, will also be inaccurate, potentially affecting business decisions.

- Importance for Decision-Making:

Accurate financial statements, underpinned by a balanced accounting equation, provide essential data for stakeholders. Investors, creditors, and management rely on accurate financial statements to assess a company's financial health. The accurate application of debits and credits ensures the underlying accounting equation is balanced, supporting informed decision-making, strategic planning, and overall financial health.

In conclusion, the accounting equation's balance is intrinsically linked to the difference between debits and credits. Correct application of these fundamental accounting tools ensures the integrity of financial records, accurate financial reporting, and ultimately, informed decision-making. The meticulous use of debits and credits safeguards the balance of the accounting equation, facilitating reliable financial statements.

6. Financial Statements (e.g., balance sheet, income statement)

Financial statements, including the balance sheet and income statement, are direct products of the accounting process. Their accuracy hinges on the precise application of debits and credits. These statements encapsulate a company's financial performance and position over a period, serving as vital tools for investors, creditors, and management. The link between debits and credits is paramount to the reliability of these statements. Understanding this connection is crucial for interpreting and using financial data effectively.

- Balance Sheet and the Accounting Equation:

The balance sheet, a snapshot of a company's financial position at a specific time, directly reflects the accounting equation (Assets = Liabilities + Equity). The asset side, listing resources, and the liability and equity sides, representing obligations and ownership, must balance. Debits and credits are fundamental to ensuring this balance. Increases in asset accounts are debited; increases in liability and equity accounts are credited. Accurate debit and credit entries underpin the balance sheet's accuracy, providing a reliable representation of a company's resources and obligations.

- Income Statement and Revenue Recognition:

The income statement, summarizing a company's financial performance over a period, relies heavily on debits and credits for accurate revenue and expense recognition. Revenue increases are credited, and expenses, which decrease equity, are debited. Correctly applied debits and credits ensure accurate calculation of net income or loss. For example, sales revenue is recorded with a credit, and the corresponding increase in cash is reflected by a debit to the cash account. Consistent application of these principles is vital for the income statement's reliability.

- Impact on Decision-Making:

Financial statements, meticulously constructed with accurate debit and credit entries, inform critical decisions. Investors analyze these statements to evaluate investment opportunities; creditors assess a company's ability to repay debts; and management uses this data to refine operational strategies. Inaccurate or inconsistent debits and credits lead to misleading financial statements, ultimately hindering informed decision-making. The accuracy and reliability of these statements are directly proportional to the proper application of debit and credit principles.

- Ensuring Consistency and Comparability:

The use of standardized debits and credits across transactions and reporting periods ensures consistent and comparable financial statements. This consistency facilitates analysis over time. For example, if a company consistently debits expenses and credits revenues according to accepted accounting principles, comparisons across different periods are meaningful. Inconsistency in debit/credit usage would create significant hurdles in accurately evaluating a company's financial performance and position.

In essence, the difference between debits and credits is a foundational element of accounting. Its accurate application is essential to the reliability and usability of financial statements. The balance sheet, income statement, and other financial reports, which distill the financial performance and position of a company, depend entirely on the precise application of these fundamental accounting concepts. Precise debits and credits underpin the transparency and integrity of financial reporting, ultimately driving well-informed business decisions.

7. Journal Entries (e.g., debit, credit)

Journal entries are the foundational records of accounting transactions. They meticulously document every financial event, using debits and credits to reflect the dual effect of each transaction. This systematic recording is crucial to maintaining the balance of the accounting equation (Assets = Liabilities + Equity). A journal entry acts as a chronological record, providing a detailed history of financial activities. The structure of a journal entry directly embodies the difference between debit and credit in accounting, forming the basis for all subsequent financial reporting.

Journal entries meticulously track changes in account balances. Each entry includes a description of the transaction, the accounts affected, and the debit and credit amounts. The difference between debit and credit is the key driver in ensuring the equation remains balanced. For instance, if a company purchases equipment for $5,000 in cash, the journal entry would debit the equipment account (increasing the asset) and credit the cash account (decreasing the asset). This careful balancing process ensures that the fundamental equation is maintained throughout all recorded transactions. Without this meticulous recording, financial statements would be unreliable and inaccurate, potentially hindering informed decision-making.

The practical significance of understanding journal entries, especially the debit and credit components, is profound. Accuracy in journal entries underpins all financial statements, including balance sheets and income statements. A single error in a journal entry can cascade through subsequent reports, leading to misrepresentations of a company's financial position and performance. Consequently, meticulous attention to detail in recording journal entries, ensuring the appropriate application of debits and credits, is crucial for accurate financial reporting. The resulting clarity allows for effective monitoring of financial health, facilitating sound investment decisions, strategic planning, and assessment of operational effectiveness. In essence, journal entries, with their debit and credit components, are the lifeblood of reliable accounting practices.

8. Accounting Principles (e.g., GAAP, IFRS)

Accounting principles, such as Generally Accepted Accounting Principles (GAAP) in the United States and International Financial Reporting Standards (IFRS), provide a framework for financial reporting. These principles establish consistent methods for recording and presenting financial information. The difference between debits and credits, a fundamental aspect of accounting, is directly influenced by these guidelines. The application of debits and credits must conform to the rules outlined in these principles to ensure accurate and comparable financial reporting.

- Consistency and Comparability:

Accounting principles mandate consistency in the application of accounting methods. Maintaining consistent debit and credit practices across various transactions and reporting periods is essential. This consistency enables comparability of financial statements over time and across different companies, allowing stakeholders to analyze trends and make informed decisions. For example, the consistent use of specific debit and credit procedures for recognizing revenue ensures that comparisons between a company's financial performance in different periods or against industry averages are meaningful and accurate.

- Matching Principle:

This principle requires expenses to be recognized in the same period as the revenue they generate. Proper application of debits and credits is integral to adhering to the matching principle. For instance, if a company incurs costs for advertising in a specific period, the related expenses should be recognized in the same period as the revenue they are designed to generate. Accurately applying debits and credits ensures that the income statement reflects the true profitability for the reporting period. Inaccurate debit/credit applications could artificially inflate or deflate reported profits, distorting the picture of a company's performance.

- Revenue Recognition:

Specific criteria govern when revenue can be recognized according to accounting principles. Accurately recording revenue through appropriate debit and credit entries is critical. For instance, revenue is often recognized when a company fulfills its contractual obligations, whether it involves delivering goods or rendering services. Applying consistent debit and credit rules for revenue recognition is vital for establishing the period in which revenue is earned and for ensuring that revenue is properly reported on the income statement, thereby upholding transparency and consistency in financial reporting.

- Conservatism Principle:

Accounting principles often dictate a cautious approach to recognizing gains and losses. The conservatism principle encourages businesses to anticipate potential losses but not unrealized gains. This principle impacts debit and credit applications when recording potential losses or liabilities. This might involve debiting a loss provision or crediting a liability account to reflect a cautious approach, reflecting potential future obligations.

In conclusion, accounting principles, like GAAP and IFRS, provide a structured framework for applying debits and credits. Their guidelines ensure consistency, comparability, and reliability in financial reporting. Adhering to these principles in the application of debits and credits contributes significantly to accurate financial statements, promoting transparency and enabling informed decision-making by stakeholders.

Frequently Asked Questions

This section addresses common queries regarding debits and credits in accounting. Clear answers to these questions provide a foundational understanding of these essential accounting concepts.

Question 1: What is the fundamental difference between a debit and a credit?

A debit increases asset, expense, and dividend accounts, while decreasing liability, owner's equity, and revenue accounts. Conversely, a credit increases liability, owner's equity, and revenue accounts, while decreasing asset, expense, and dividend accounts. This duality ensures the balance of the accounting equation (Assets = Liabilities + Equity).

Question 2: How do debits and credits affect the accounting equation?

Every transaction recorded in accounting affects at least two accounts. A debit in one account is always accompanied by a corresponding credit in another. This ensures that the total debits always equal the total credits, maintaining the balance of the accounting equation.

Question 3: What is the importance of correctly applying debits and credits?

Correct application is essential for accurate financial statements. Inaccurate entries can lead to misrepresentations of a company's financial position and performance. This, in turn, can impact decision-making by investors, creditors, and management.

Question 4: Can you provide a simple example illustrating the use of debits and credits?

If a company purchases supplies for $100 in cash, the supplies account (an asset) increases, requiring a debit. Simultaneously, the cash account (another asset) decreases, requiring a credit. These entries reflect the dual effect of the transaction and ensure the accounting equation remains balanced.

Question 5: How do debits and credits relate to financial statements like the balance sheet and income statement?

The balance sheet's accuracy depends on correct debits and credits, as it reflects a company's assets, liabilities, and equity. The income statement utilizes debits and credits to record revenues and expenses, facilitating the calculation of net income or loss for a reporting period.

A thorough understanding of debits and credits is fundamental to accurate financial reporting and effective business decision-making. This knowledge underpins the reliability of financial statements, enabling stakeholders to make informed judgments about a company's financial health.

Moving forward, let's explore more complex accounting topics.

Conclusion

The difference between debit and credit in accounting is a fundamental concept. Accurate application of these principles is crucial for maintaining the integrity of financial records. This article explored various facets, including account types (assets, liabilities, equity), transaction impacts (purchases, sales), and the vital role in upholding the fundamental accounting equation. The interplay between debits and credits directly impacts the creation of financial statements such as the balance sheet and income statement. Understanding this interplay is essential for stakeholders, enabling informed decision-making and assessing a company's financial health. The consistent application of debits and credits, in accordance with established accounting principles, ensures reliable financial reporting. Inconsistencies in application can lead to inaccurate representations of financial status, impacting investor confidence and potentially jeopardizing sound business practices.

In conclusion, the difference between debit and credit is more than a bookkeeping technique; it's a cornerstone of accurate financial reporting. A profound understanding of this concept is essential for anyone involved in business operations or financial analysis. Mastering this fundamental aspect of accounting allows for a clear and reliable picture of an organization's financial performance and position, fostering trust and transparency in financial markets and facilitating sound decision-making within businesses.

Article Recommendations

- The Political Views Of Travis Kelce Insights And Revelations

- Did Dr Pol Retire

- Gigi Ulala Fun Facts Latest News

:max_bytes(150000):strip_icc()/dotdash-050415-what-are-differences-between-debit-cards-and-credit-cards-Final-2c91bad1ac3d43b58f4d2cc98ed3e74f.jpg)